6 exercises to stress-test your Midlife Gap Year

If you’ve let yourself dream about taking a Midlife Gap Year, you may stop your planning as soon as the “What if…” questions kick in. Even with accumulated nest eggs of a few million dollars, many successful midlife business owners and leaders fear potential negative outcomes of taking this desired career break. The best way to see if you can tolerate the trade-offs necessary to make your Gap Year a reality is to stress test the idea against the worst-case scenarios.

The following six exercises are designed to help you determine if your current personal and financial situations are ready for this time away from work and what that might look like.

Exercise 1: Project income during your Midlife Gap Year

Complete the following chart to outline your sources of income. Fill in the amount of income you expect to receive under each column. We have provided a few sample numbers to illustrate.

* Be sure to include any lost income during “re-entry” in this calculation, too.

As you fill in the chart, consider the following questions:

- Will you continue to receive income from your business? If so, will that amount change or stay the same? If your business income is generated based on a percentage of sales or commissions, it’s best to calculate with the minimum amount you would expect to receive to avoid overcasting your budgeting net.

- Will there be a project you will be paid for during your break?

Once you have completed this exercise, you will be able to see how much your income may change. This will help you determine your financial need for the Gap Year. If you do not expect to make any business or salary income based on the nature of your work and your chosen Gap Year adventure, then you simply tally up any other income streams you may receive. * Be sure to include any lost income during “re-entry” in this calculation, too.

Exercise 2: Calculate expenses during your Midlife Gap Year

Identify how your expenses may change during the break. Use the following chart to help you outline your changing need.

Items to consider:

- Will you be able to retain health insurance and other benefits during your Gap Year? Or will you need to buy additional coverage?

- If you are considering going overseas for a year or more, you may consider selling your car to fund alternative transportation abroad or invest in your trip. Or, if you won’t be using your vehicles but you want to hold on to them, you may be able to negotiate or purchase a lower insurance policy for the interim you are away.

- The biggest expense you may carry is likely your home. Are you open to renting it out while you’re away? Or do you prefer to keep it unoccupied? Are you ready to sell or willing to consider it?

Exercise 3: What is your Midlife Gap Year financial need?

Determine how much you will need beyond your ordinary income to pay for the Gap Year using the numbers generated in Exercises 1 and 2.

If your final need is positive, chances are you can afford to take your Gap Year without significant funding or investment from other sources. Skip Exercise 4 and move into Exercise 5.

If, however, your number is negative you will need to decide how you will come up with the funds necessary to make your Gap Year a reality. Move on to Exercise 4.

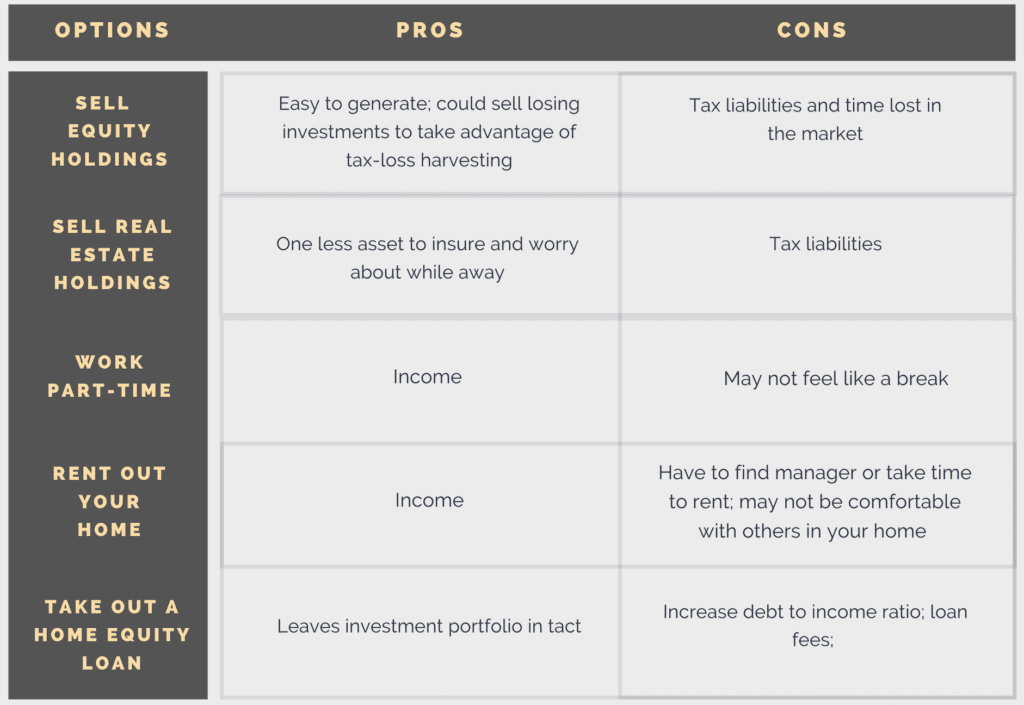

Exercise 4: Funding your Midlife Gap Year

Determine how you will raise the amount to fill “your need” in Exercise 3 from other sources.

If your Gap Year planning aligns with an upcoming sale of your business or other significant liquidity event, then you can take a look at how much you are willing to invest from the proceeds to take the time off.

If not, then this is where your creativity and financial savvy will come into play. You will have to first identify sources of income you could use to fund this investment and then weigh the merits of each choice to make the right decision.

For example, you could liquidate some investments or take a loan out against them to jumpstart your Gap Year. Or, you could work part-time while on your break to earn extra income. You could consider renting out your home while you are away or even selling your vehicle to give you the cash you need. More dramatic options include downsizing your home or borrowing against it.

Review the chart below to identify the pros and cons of each option.

Exercise 5: Trade-offs for the Midlife Gap Year

Create a list of trade-offs you may have to make to take a Midlife Gap Year. Divide the list into two columns: personal trade-offs and financial trade-offs.

Some examples may include postponing other priorities such as an early retirement, buying a second home, taking fewer vacations when you return, or cutting back expenses in another area. You may trade-off a feeling of employment security if you need to find a new job or have to ramp back up again upon your return. If you have to sell other investments, include this in your list.

Exercise 6: Make a list of worst-case scenarios and do a gut-check

If you’ve come this far, it’s likely you see the value in taking a Gap Year and want to reap the benefits of this opportunity. But, there might still be something holding you back.

Here is the juncture where you will make a list of the worst-case scenario results of taking a Gap Year and gut-check those “what ifs” against your own personal risk tolerance.

If you have a partner, it might be helpful to volley these worst-case scenarios back and forth with one another, talk through the possibilities, and theorize how you would handle them if they arose.

Then, see how you feel about these scenarios:

- Do you feel more or less confident about taking a Gap Year after completing these exercises?

- Do the trade-offs give you any type of physiological responses, positive or negative? For example, can you feel your blood pressure going up at the thought of having to liquidate another investment to fund your year? Or, does the idea of maintaining your hectic pace of life make your stomach turn?

- Speak with your spouse. How do they feel about financial realities and trade-offs outlined in these exercises?

If a full Gap Year doesn’t sit right or seems to far out of reach, repeat these exercises with a shorter time frame in mind or a break with a less cumbersome financial ticket attached. You can reuse this template as many times as you like for different scenarios until you find one that works for you.

Planning for a Gap Year is not a new idea, but is one that hasn’t been widely exercised by business owners until more recently. It is only natural to have some trepidation. By stress testing possible outcomes, you can make an informed decision about what type of break makes the most sense for you and set yourself up to reap the benefits of an extended break.

Not sure if your logic or intuition are guiding you in the right direction?

This is where we can help. We guide business leaders through a 3-step process that includes thorough scenario planning and explores the impact these trade-offs might have on your personal and financial well-being.

Schedule an introductory call with one of our advisors to discuss if a Gap Year could be right for you.

In the meantime, download our MidLife Gap Year Guidebook that outlines the process and benefits in more detail. We look forward to helping you take the next step!

The information provided herein is for informative and educational purposes only. The use of hyperlinks to third party websites is not an endorsement of the third party. Third party content has not been independently verified. To understand how this content may apply to you, please contact a financial advisor.