The Gen X Dilemma (Part 2): How Do You Talk Finances With Aging Parents?

Conversing with aging parents

In Part 1 of this series we reviewed the pressures you experience as parents. Now in Part 2, we’ll touch on the ones you experience from parents. That is, the financial and emotional stress that comes along with your ever-aging mom and dad.

If the pandemic reminded us of anything, it’s that life is precious. And the older we get, the more vulnerable we become. So those financial conversations we have with our parents can’t be put off. They need to happen sooner rather than later. [As I mention in an interview with thebalance.com on this topic, “There is no shortcut to having these discussions, which may be difficult—or at least awkward—in most family dynamics.” ]

Together we’ll go over the questions to consider as you enter into a financial dialogue with your aging parents. Keep in mind that conversations around finances and end of life are touchy to say the least. So make sure you approach them from a place of openness and respect.

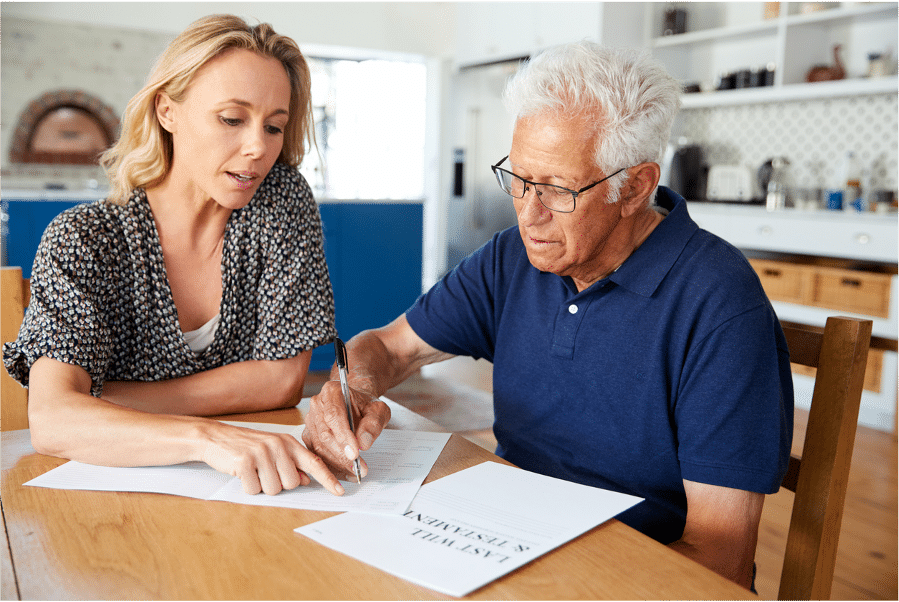

What documents do I consider?

You’ll want some of your conversations in writing. In fact, there are several documents you’ll want gathered to make life easier on you and your parents. These documents include, but are not limited to:

- Trusted Contact: Your parents have the option of naming you as a trusted contact on their investment accounts. This authorizes their financial firm to contact you under certain circumstances. It’s essentially a fail safe where you’ll be alerted of suspicious activity should your parents be unable to reach.1

- Authorized Agent: If your parents name you an authorized agent, your access is furthered. With this, you’ll be able to access their investment account and even place trades. However you will not be able to access or transfer funds. Again, this can be a great way to keep an extra eye out for unusual activity.

- Financial Power of Attorney (POA): With financial POA, your parents can give full authorization to make financial decisions on their behalf. “Durable” forms of POA remain intact even if your parents become medically or cognitively incapacitated. And a “springing” POA allows for the authority to be given at a point in the future after signing.2

- With no POA in place, the court process of conservatorship determines who makes these decisions for your parents should they be unable to. But appointing a Conservator is lengthy, complex, and expensive. There’s also no guarantee who the court will appoint as Conservator, so it’s best to have your parents sign a springing Durable POA in advance, while they have full cognitive function.

- Living Trust: This document is for the transference of your parents’ assets. It names a trustee, or co-trustees, who will manage the assets until they reach the designated beneficiary. Without a living trust in place, your parents’ assets will be subject to the probate process. This court proceeding can be complicated and costly, and slow down the transfer of your parent’s wealth.

TIP: When your parents are choosing their authorized agent, trustee, or trusted contact, they can apply our “core four” criteria. These are: aptitude to help, interest to help, time to help, and proximity to help. Suffice to say, their choice should be wise, engaged, flexible, and nearby.

Should I intervene financially?

Whether or not you should intervene financially will depend on your parents’ situation. But you can’t intervene if you can’t see the problems. Below is a list of ways to collaborate with your parents to ensure their wealth stays on track:

- Review Their Bills: It’s worthwhile to have transparent access to your parents’ expenses. This will show not only if bills are being paid on time, but that there aren’t also unnecessary charges. We’re all susceptible to losing track of our subscriptions, but it only becomes more common with age.

- Credit Cards And Utilities: Speaking of bills, let’s touch on credit cards and utilities. You’ll want to make sure both your parents are set to make payments. That way, if one passes, the payments will continue uninterrupted.

- Tax Prep: The last thing your aging parents need is an audit. It’s worth checking in to make sure they’re on top of filing, record keeping, and aware of any changes that would affect what they owe or deduct. For example, in California, pensions are fully taxed, but Social Security benefits are exempt aside from a 2.5% tax on early distributions.3

What should I brace for?

We may not like to think about it, but with age comes loss. Even before death, mental and physical capacity decline. Preparing for the changes that come with these losses can bolster your family emotionally and financially. Brace yourself for the following:

- Loss of Driver’s License: Research from Columbia University revealed that the elderly who stopped driving declined faster physically and cognitively, saw major reductions in their social circle, and were significantly more likely to move into an assisted living community or nursing home.4 If your parents lose their license, the support they need will likely extend well past occasional car rides.

- Loss of Competence: Taking your parents’ competence for granted is a mistake. Like everyone, your parents are allowed to make bad decisions, and it is sometimes difficult to tell if this is due to diminishing competence. You should be prepared for this to be a process, not necessarily occurring at a set point in time. But regardless of its design, a Durable Power of Attorney must be in place before any loss of competence. Otherwise, you may be subject to a court process.

- More Doctors Appointments: The need for routine health check ups increases with age. The CDC found that those over the age of 65 visit the doctor more than twice as often as those aged 18 to 44.5 For this reason, it’s critical to examine the most cost-effective health plans for your parents and, if possible, have someone accompany them to the visits to confirm information and follow-up.

- End of Life and Estate Plan: The last thing you need in a time of grieving is more to worry about. If you are named to serve as Power of Attorney for Healthcare, be sure that you understand your parents’ end of life wishes. Final decisions about prolonging care will rest with you and this difficult task will be eased if you are confident you are carrying out their wishes. You will also want to ensure that your parents’ estate is in order. So review documents (wills and trusts) and designations (trustees and beneficiaries) ahead of time. Otherwise, the legacy they leave behind will involve a bumpy process instead of a smooth one.

What about changes in living arrangements?

Depending on your parents’ condition, adjustments to their living arrangements may be necessary. These scenarios often involve:

- Moving Or Downsizing: Whether it’s reducing upkeep, unneeded space, or flights of stairs, it can make sense to relocate. Plus, getting closer to the grandkids and having some cash from a fresh home sale are usually huge wins for your parents.

- Moving In With You: Allowing your parents to move in with you takes a major financial burden off their shoulders. And they’ll be closer to loved ones in their time of need. However, this arrangement isn’t suitable for all family dynamics. A clearcut discussion of expectations may be necessary before pursuing this option.

- Assisted Living: If your parents struggle with disabilities, or would simply prefer not to live by themselves, they may consider assisted living. These are often communities meant to be more “homey,” as each resident lives in their own apartment with kitchen appliances. But this option can get expensive. It was found in 2020, that the average cost of assisted living in California was $5,000/mo.6

- Nursing Home: This option is much more hands-on and expensive. Your parents would likely be staying in a private (or semi-private) room with no kitchen appliances. And in California, the average cost for nursing homes has been found to be between $9,247 and $11,437/mo.6

- Stay At Home (Accommodations): It’s common for parents to want to “age in place.” But that may only be possible with installation of various home accommodations. These may include, but are not limited to walk-in showers, shower rails, stair lifts, or new flooring. Additionally, if you’re looking for an in-home care provider, expect around $6,101/mo in California.7

(Bonus) What technological resources are at my disposal?

You’re not alone in facing worry over your older parents. Several technological advancements have been made to help calm concerns. It may be worth checking out the following:

- Wearables: Whether it’s a Fitbit, Apple Watch, fall detector, or heart monitor, several high-tech wearables make monitoring well-being easier, and even stylish.

- Auto Pill Dispensers: Companies like Hero Health have revolutionized taking your meds. Their automatic pill dispenser and proprietary app make scheduling, ordering, and taking prescriptions completely automatic and routine.

- Alexa Together: Amazon’s Alexa Together service offers Amazon Echo users peace of mind. That’s because features like fall detection, activity alerts, and a 24/7 emergency hotline are offered to caregivers to support their aging loved ones.

- ElliQ: Over at ElliQ, senior socialization has been made a priority. Their voice-operated, virtual companion makes it easier than ever to book Uber rides, remember birthdays, make video calls, set goals, and stay integrated within relationships.

How The Advisory Group can continue to help

We partner with clients through thick and thin. We’re here to help you as your kids are launching into the world, and your parents are navigating their golden years.

Talking about the financial and physical complications that come with old age can be overwhelming. Especially when it involves your loved ones who’ve been independently functioning for decades. Nevertheless, it’s a conversation that needs to happen.

If you’re ready to do right by your folks, we’re ready to lend our expertise. Our team is here to strategize on how to best provide for your parents while also keeping your midlife financial plan in tact. You can get started by setting up your complimentary consultation, or calling us directly at (415) 977-1200.

References:

- https://www.finra.org/investors/learn-to-invest/brokerage-accounts/establish-trusted-contact

- https://www.law.cornell.edu/wex/springing_durable_power_of_attorney#:~:text=A%20power%20of%20attorney%20is,after%20the%20principal%20becomes%20incapacitated

- https://www.sambrotman.com/blog/tax-help-for-seniors

- https://www.stellartransport.com/new-research-finds-correlation-senior-health-loss-drivers-license/#:~:text=81%25%20of%20adults%20in%20the,safely%20drive%20and%20navigate%20roads

- https://www.aarp.org/health/conditions-treatments/info-2019/how-often-you-should-visit-doctor.html#:~:text=En%20espa%C3%B1ol%20%7C%20Health%20problems%20that,for%20Disease%20Control%20and%20Prevention

- https://rosewoodseniorlivings.com/how-much-does-assisted-living-cost/

- https://www.genworth.com/aging-and-you/finances/cost-of-care.html

The information provided herein is for informative and educational purposes only. The use of hyperlinks to third party websites is not an endorsement of the third party. Third party content has not been independently verified. To understand how this content may apply to you, please contact a financial advisor.