Smart spending policy for endowments: How to avoid corpus erosion and fulfill your fiduciary responsibility

Endowment fiduciaries are amazing people, sharing their time, and often financial resources, for the benefit of a larger goal for their communities. Many endowment committees of funds under $100 million, and especially under $50 million, however, are not fully optimizing their outcomes. This can be due to gaps in their fiduciary, spending policy or investment policy processes. This article focuses on the spending policy component.

[To see how Spending Policy fits within endowment fiduciary responsibility more broadly, and the regulatory framework for endowments (UPMIFA), see our “Endowments 101” article.]

Spend to maximize impact without eroding corpus

Endowments are vital for accomplishing the desired community impact of many non-profits, as well as the long-term financial health of those institutions, including foundations, universities, and other not-for-profit entities. A critical aspect of managing an endowment is maximizing impact by setting a prudent spending policy that aligns with the organization’s goals, needs, investment policy and fiduciary responsibilities. The policy must not inadvertently shrink the “corpus” or purchasing power of the pool of assets, or violate other fiduciary requirements.

Before developing a spending policy, it is important to understand that not all entities thought of as endowments are actually true endowments. The spending policy implications can be very different. An endowment’s categorization depends on the nature of the funds and how they were contributed, and important fiduciary guidelines vary accordingly.

How true endowment spending can be different than quasi-endowments

A true endowment is a fund where donors specifically designate the funds to last into perpetuity, which can occur by the donor labeling the funds as an endowed gift, or if the organization overseeing the funds labels the donations, sometimes incorrectly, as an endowment. Funds categorized as an endowment may spend from the assets, but only using a carefully crafted, documented and prudent spending policy, to ensure the donation or “corpus” maintains an inflation- and cost-adjusted value over time. Determining spending levels based on investment income or investment gains is not an appropriate spending method.

Endowments have different treatment under the regulatory guidelines versus quasi-endowments (which are also known as board-endowed funds). Quasi-endowments are generally funds not declared to be “endowed” funds by the donor or endowment fiduciaries, and therefore do not have perpetuity requirements or spending restrictions, unless otherwise required. Endowment fiduciaries, however, treat the funds like an endowment to maintain corpus and inflation-adjusted purchasing power over time.

Fiduciaries that wish to have greater flexibility regarding their spending are advised to fundraise in a way that doesn’t make “endowed” status the default or only option to donors. They should avoid labeling non-endowed funds as endowments in documentation to avoid inadvertently subjecting the funds to the more restrictive endowment regulatory requirements.

With the above clarified, the information below will focus on spending policy concepts for endowed funds which can also often be the best practice for quasi-endowed funds.

The role of UPMIFA in spending policy

The Uniform Prudent Management of Institutional Funds Act (UPMIFA) is the current regulatory framework for endowments, and has been adopted by the vast majority of US states. UPMIFA establishes fiduciary guidelines for managing most non-profit funds, including endowment funds. Part of that fiduciary framework for funds designated as endowments includes seven factors that should be considered in developing a spending policy:

- Preservation of the fund

- Purpose of the endowment

- Expected total return from investments

- Effects of inflation

- General economic conditions

- Other resources of the organization

- Investment policy of the endowment

It is important to note that costs related to managing and maintaining an endowment are also part of fiduciary responsibility. Costs should be a factor in a spending policy analysis and should be monitored and reasonable.

Spending policy development

UPMIFA spending guidelines are general in nature, and do not provide a specific method for determining a spending calculation. Utilizing an appropriate process and data inputs to a spending policy formula is critical to fulfilling endowment fiduciary responsibility.

Spending policy approaches

The Implied Spending Method and Required Return Method are two distinct approaches to developing endowment spending policies, each with its own set of characteristics and implications.

Implied spending policy

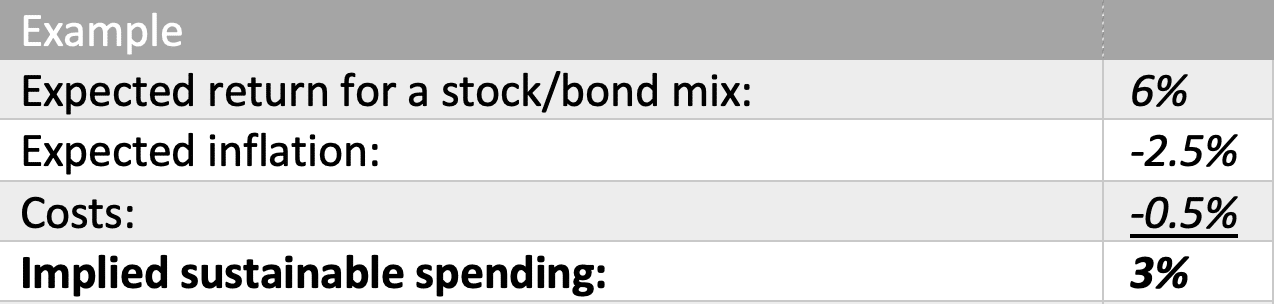

The Implied Spending Policy Method starts with the use of a defensible expected return of a given stock/bond mix as the key variable, and then subtracts expected inflation, and costs, as well as subtracting or adding other relevant variables, to produce a reasonable spending number as an output of the formula. If done appropriately, the Implied Spending approach produces an annual spending rate that should be sustainable until the key inputs change materially, at which time the formula should be updated. This method can require an iterative process to determine alternative spending and stock/bond Investment Policy mix scenarios.

For example (hypothetical data):

This method produces a usable output if the inputs are sufficiently complete and reasonable, and if those variables are updated as the projected variables evolve over time.

Required Return Approach

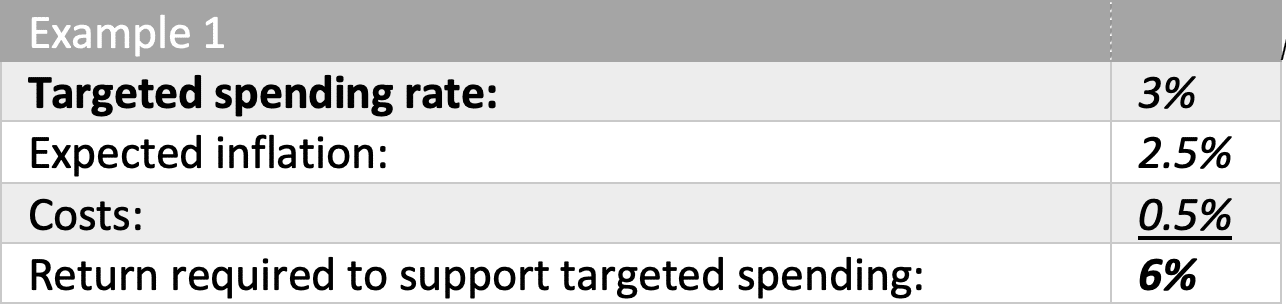

The Required Return Spending Policy Method begins with a goal spending rate, and then adds expected inflation and costs, as well as subtracting or adding other relevant variables, to determine the level of investment return required to sustain the targeted spending level.

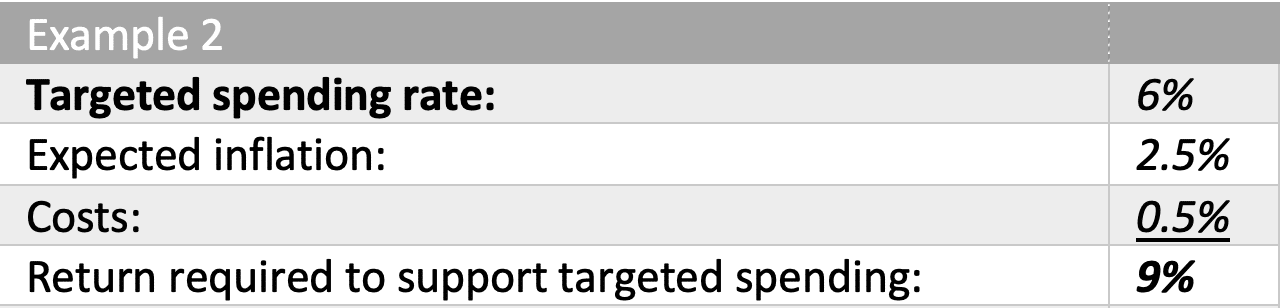

For example (hypothetical data):

As noted above, in Example 1, the Required Return Method can lead to the same conclusion as the Implied Return Method.

Example 2, however, illustrates inputs that lead to an impossible required return output under relative to current long-term capital market expectations, even if a 100% stock portfolio were utilized. This expectation would lead to systematic corpus erosion as well as exceeding the risk and spending variability tolerance of most fiduciaries and entities.

Both spending policy development methods above are simplified for illustrative purposes and exclude important potential additional variables and rely on hypothetical numbers. Appropriate spending policy formulas should rely on carefully crafted expectations regarding inflation, capital markets returns and other variables, several of which may be specific to each entity, sometimes including specific inflation measures that might be more directly related to the endowment’s targeted impact.

Proper spending policy makes investment policy decisions easier

Used properly, spending policies increase the probability of prudent spending, reduce the chance of corpus erosion, and make an endowment fiduciary’s job easier. By using a spending policy analysis process, and applying a spending smoothing rule, rather than relying on guesswork, spending and investment policy becomes easier and more effective.

Another benefit of a solid spending policy process that utilizes reasonable and defensible expected portfolio return assumptions for an array of stock/bond mixes is that it helps fiduciaries choose an appropriate stock/bond mix. A given spending policy is associated with a specific expected return, which is associated with a specific stock/bond mix, thereby connecting spending policy to investment policy.

The key is to use a process that aligns the spending policy with the organization’s overall mission, risk tolerance, and investment strategy to ensure the long-term sustainability of the endowment fund.

Smoothing rules

Prudent endowment spending requires more than an appropriate spending formula calculation. Given that investment markets can be volatile, the simple application of a spending rule could create dramatic variability in actual spending on a year-by-year basis. Such spending inconsistency can be especially problematic for endowments that intend to provide consistent funding to their grant recipients whose programs rely on specific dollar levels from an endowment for the grant recipient to function.

To reduce this underfunding risk, “smoothing rules” are often applied. An array of spending smoothing methods exist. One example averages the market value of the endowment over a number of years before applying the spending rule.

Other spending and non-spending restrictions

Special donor-imposed restrictions

Some donors to endowments establish restrictions beyond the basic spending limitations implied and required by designating funds as an endowment. For example, a donor may require that particular dollar amount be spent by a certain date, or a particular dollar amount or percentage spent each year, or combination of the above.

Such spending restrictions may override and therefore complicate the normal corpus erosion avoidance spending policy expectations of UPMIFA and may be in conflict with a donor’s simultaneous expectation that the funds will last into perpetuity. Organizations that have clear and prudent spending policies are better able to educate donors regarding how the donor’s restriction requests may conflict.

Spending from income vs. from total-return

Another spending policy complication can arise when donors require that money only be spent from “income.” An “income-only” approach was considered a best-practice decades ago as a way to reduce or avoid corpus erosion, but an income-only approach may under- or over-spend, and can lead some well-meaning fiduciaries to design an investment portfolio so that it maximizes “income,” but often times with significant expected return reduction and/or increased risk, through lower diversification. The current best-practice is no longer an “income-only” approach, but rather the use of a prudent spending policy that utilizes a total portfolio return approach within the spending policy analysis.

Spending above a spending policy and/or above UPMIFA’s max assumed level

Spending above a spending policy level should not be a regular practice, but UPMIFA does allows for spending above a spending policy in certain circumstances. It is advisable to consult a non-profit/UPMIFA attorney in such cases.

Also, most states, including California, have adopted the optional UPMIFA provision stating that spending above 7% of an endowment (using a 3-year average market value) is presumptively imprudent. This does not mean, however that any spending level under 7% can be presumed prudent, rather spending policy should be based on a defensible method, such as those outlined above.

Restrictions that can indirectly impact spending

Well-meaning endowment donors may also establish restrictions that do not directly impact spending policy, such as security types, security quality levels, and other limitations; however, this can also decrease diversification. Less diversification can decrease expected return and increase risk and indirectly impact spending policy. Such investment restrictions can also complicate the work of endowment fiduciaries, and involve higher operational or portfolio costs. Again, donor education is key to reduce restrictions that might actually work against the donor’s highest goals.

When a spending policy does require a design for perpetuity

While uncommon, donors can define the period of time over which their endowment gift endowment can be spent. Such endowment gifts are known as term endowments, and this is the only type of endowment funding that can be spent down rather than retained in perpetuity.

Spending “underwater”

Unlike UMIFA (the Uniform Management of Institutional Funds Act), the predecessor framework to UPMIFA, UPMIFA allows organizations to spend from “underwater” endowments if the fiduciaries determine it is prudent to do so. Underwater funds are those where the fund value drops below the corpus, for example due to market volatility. If spending levels are prudent and fiduciaries consider reasonable long-term return averaging assumptions, spending is allowed. Over-spending in underwater cases can accelerate corpus erosion, however, so it may be prudent for fiduciaries to consider spending reductions or pauses, especially if doing so is not excessively detrimental to the organization’s mission.

How to reconcile large planned spending with spending policies

When a non-profit entity’s assets include unrestricted money that can be fully spent at any time, unlike endowment assets, or there are unspent but spendable endowment assets (accumulated over time and “banked” for future spending), some endowment fiduciaries may allowably choose to spend larger lump sums in order to further their missions, rather than grow corpus and use a spending policy as a guide for unrestricted assets.

In those cases, it is generally appropriate to maintain separate portfolios with different time frames, to minimize the impact of volatility on assets that have a shorter time frame. For example, there might be a long-term fund, a medium-term fund, a short-term fund, and an ultra-short-term fund, to address such spending timing, to optimize return and minimize risk. Other time-frame based portfolios are less common, but sometimes appropriate.

How to plan for future spending is decades away?

While less common, some endowments or endowment-like funds have “ultra-long” time frames. This may involve a period of decades with a corpus growth focus and no spending before a spending policy begins. In this type of situation, a “glidepath” approach to investing may be appropriate, starting with a higher stock, higher volatility portfolio to maximize growth, followed by a schedule to gradually reduce the stock allocation and increase the bond allocation. This dynamic asset allocation approach can be done programmatically until the year spending is projected to begin, and then stock/bond mix would then be set to match the corresponding expected return dictated by the spending policy.

Should spending policies be adjusted for short-term market conditions?

Prolonged periods of higher or lower returns compared to long-term return projections may tempt endowment fiduciaries to make temporary adjustments to spending policies to increase spending, avoid perceived underspending or decrease spending to avoid corpus erosion.

To the extent that fiduciaries are concerned that smoothing rules will not be sufficient to address market variability dynamics, short-term spending reductions in spending may be advisable when markets experience prolonged downturns. With the exception of private endowments that currently have a minimum legally mandated 5% minimum spending rule, public endowments are not limited to spending less than their normal spending policy unless a donor has specified a particular spending rate.

When portfolio returns experience prolonged periods above the expected return, fiduciaries might treat money from excess investment returns as banked excess unrestricted funds. However, fiduciaries should be careful not to over-spend in a way that fails to recognize that market returns tend to revert to the mean over time. Heavier spending now could unintentionally increase the possibility of corpus erosion later, if a strong market cycle swings to a prolonged weak market cycle.

Additionally, UPMIFA does provide for spending above normal spending policy levels in some cases, when sufficiently justified. In such cases, documentation of the rationale relative to UPMIFA-allowable exceptions is important, and the guidance of an attorney in such cases is advisable to avoid fiduciary and/or corpus risk.

Spending policy summary

Developing a spending policy for an endowment is a critical element of a proper endowment management process, and requires a delicate balance between preserving the fund’s corpus for the long term and fulfilling the organization’s mission in the short and long terms.

Fiduciaries can more successfully fulfill their responsibilities by carefully:

- considering the factors outlined in UPMIFA and the key variables not specifically defined by UPMIFA,

- choosing the right approach between Implied Spending and Required Return methods,

- using prudent and defensible variables as inputs to spending policy analysis formulas, and

- implementing effective spending smoothing rules,

A prudent and effective spending policy development process also relates to prudent investment policy development. A coordinated spending and investment policy process makes the job of fiduciaries easier, and their organizations can ensure that endowment funds remain a robust, sustainable resource to accomplish their missions into the future.

If you’re an organization with an endowment you’d like to secure, we can help. To have a conversation about how to get your endowment fiduciary process to the next level, contact us.

The information provided herein is for informative and educational purposes only. The use of hyperlinks to third party websites is not an endorsement of the third party. Third party content has not been independently verified. To understand how this content may apply to you, please contact a financial advisor.